Credit is a system. And like all systems, it can be redesigned.” — Hernando de Soto

The global credit gap is not a mystery. It is an architecture failure.

Five hundred million entrepreneurs worldwide operate real businesses. They employ people. They serve customers. They generate revenue. But fewer than five percent of them have access to formal credit. Not because they are risky. Because the systems built to measure risk were never designed to see them.

Traditional credit scoring relies on bank statements, tax filings, and credit bureau histories. In markets where eighty percent of commerce is informal, those inputs do not exist. The result is not a lack of creditworthy borrowers. It is a lack of infrastructure to identify them.

I did not learn this in a textbook. I learned it by lending four million dollars into small businesses that every bank had refused — and getting every dollar back.

The Financial System is Broken for Small Businesses

The financial system is not broken for everyone. It works precisely as designed — for the populations it was built to serve. Large banks in developed markets have sophisticated risk models, vast datasets, and regulatory frameworks tuned to their customer base.

The problem is that those models were never exported. And the institutions that could have adapted them chose not to. Serving a small-business owner in a developing market requires different data, different risk models, and different unit economics. Most banks looked at that equation and walked away.

What they left behind was not just a market gap. It was a structural vulnerability. When ninety-five percent of entrepreneurs in a region cannot access capital, you do not have an economy. You have a lottery. And lotteries do not build nations.

The Experiment

At StorsApp, we decided to prove the thesis with capital, not theory.

We built an AI-powered credit scoring engine that uses alternative data — purchase histories from our RxAll pharmacy network, supplier payment records, transaction velocity, business tenure, and community trust signals. We trained models to identify creditworthy businesses that traditional systems could not see.

Then we raised capital through the Stors token on Solana. We gave US retail investors a direct, transparent vehicle to deploy working capital into high-quality small businesses globally. The structure was simple: investors provided capital, borrowers received working capital loans, and the platform managed origination, servicing, and collections using AI.

The results over two years:

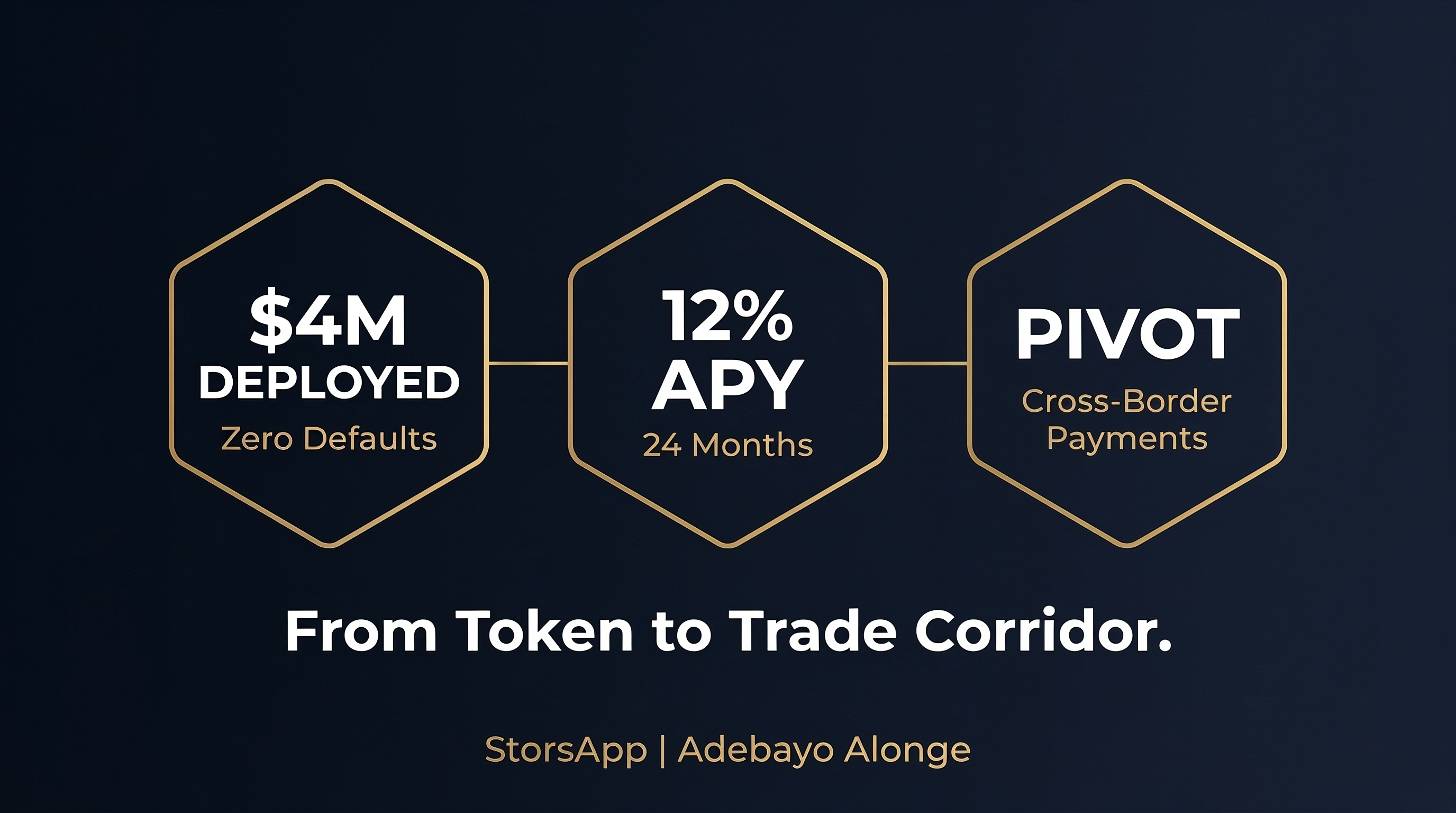

A. Four million dollars deployed into small businesses across markets where formal credit penetration was below five percent.

B. Zero default rate. Not low. Zero. Every dollar returned.

C. Twelve percent annualized yield to investors — outperforming most fixed-income instruments available to retail investors.

D. Ninety-nine point five percent borrower retention over twenty-four months. Businesses did not just borrow once. They came back. Because the capital worked.

E. Six million dollars in lending volume closed with enterprise-level asset managers who saw the data and wanted in.

After two years, we returned every dollar to our token investors. The experiment was complete. The thesis was proven.

The Pivot

But the experiment revealed something we did not expect.

The businesses that performed best were not just borrowing to stock inventory. They were borrowing to sell across borders. A pharmaceutical distributor buying certified medicines through RxAll to sell into a neighboring country. A food processor buying raw materials locally and shipping finished goods to an importer three markets away.

The real constraint was not capital. It was trade infrastructure.

Small businesses in developing markets cannot easily receive payments from international buyers. They cannot navigate cross-border compliance. They cannot access the trade finance instruments that multinationals use as a matter of course. The payments rails that connect a factory in Ohio to a buyer in Hamburg simply do not exist for a manufacturer in Lagos trying to reach a retailer in Accra.

So we pivoted. StorsApp is now a cross-border payments and trade finance platform for small businesses. We enable entrepreneurs in developing markets to tap into export markets — processing payments, managing compliance, and providing financing to those with verified export flows on our platform.

The lending engine remains. But it is no longer standalone. It is embedded inside a trade corridor, financing the businesses that are already moving goods and earning revenue across borders. The risk model is stronger because we finance real flows, not projections.

Capital without borders is the future

The opportunity is staggering. Cross-border trade among small businesses in developing markets is estimated at over three hundred billion dollars annually — and growing. Most of it moves through informal channels because formal infrastructure does not serve businesses at that scale.

We are building the formal channel. AI-powered. Compliance-embedded. Financed by real flows.

This is not financial inclusion as philanthropy. This is financial architecture as competitive advantage. The companies that build trade corridors for the five hundred million underserved entrepreneurs will capture value at a scale that traditional banks chose to ignore.

Capital without borders is not a theory. It is a blueprint — and we built it.

Onwards.

Adebayo Alonge is the Founder and Group CEO of the RxAll Group. A Harvard Kennedy School Mason Fellow, Yale School of Management alumnus, and MIT Legatum Fellow, he builds AI-powered platforms that deliver healthcare, capital, and clean energy to underserved markets worldwide. He has raised $11M+ from Tier 1 VCs, driven $180M+ in product sales, and serves millions of patients monthly. He is a Fast Company World Changing Ideas 2025 honoree and winner of the Hello Tomorrow DeepTech Prize.

Discover more from Adebayo Alonge

Subscribe to get the latest posts sent to your email.